Cornhusker Economics January 27, 20162016 Cow-Calf Production Shows Less Profitability

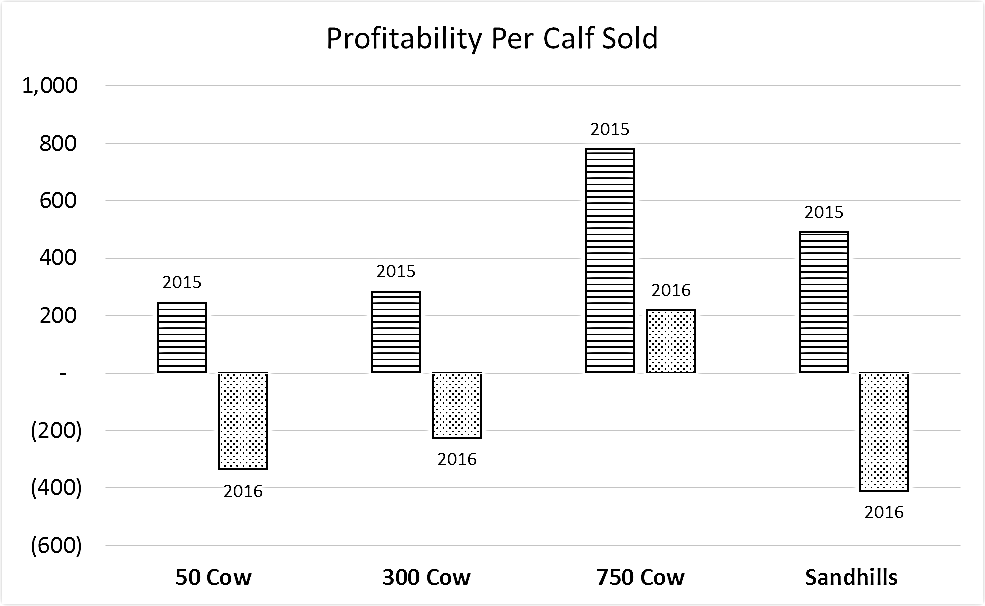

In 2015 the University of Nebraska Agricultural Economics Department formulated four cow-calf budgets. The Sandhills cow/calf producer budget is for a herd of 500 cows and the data is from a panel of producers in Cherry County. The remaining three budgets are the 50-cow herd located in the panhandle of the state, and 300- and 750-head cow herd systems generally located in and around Custer County. These last three budgets were compiled from producer survey data collected for this purpose. Budgets are available online at the UNL Farm and Ranch Management website.Cattle and feed prices have recently been updated for 2016. These updated budgets show that profits have declined in every budget group compared to the 2015 budgets.

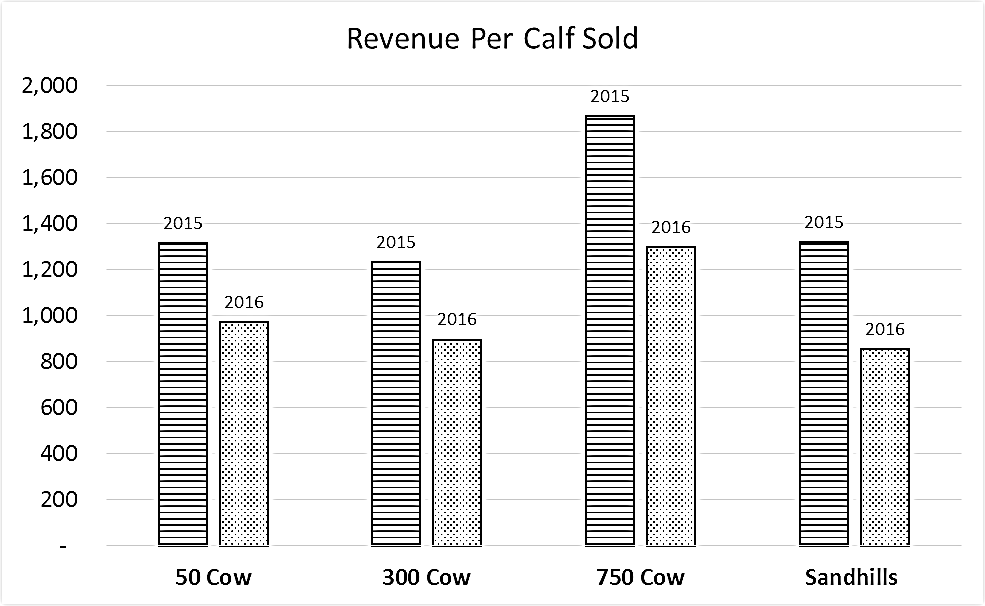

These declines in profitability are partly the result of a reduction in gross incomes. Revenues from 2016 cattle sales range from 65% to 74% of those in 2015. The large disparity of revenue decline among the various budgets is partly due to time lag in the preparations of the 2015 budgets, which occurred during a time when prices declined. The 2015 Sandhills Cow/Calf Producer Budget was completed nearly 50 days before the other three budgets.

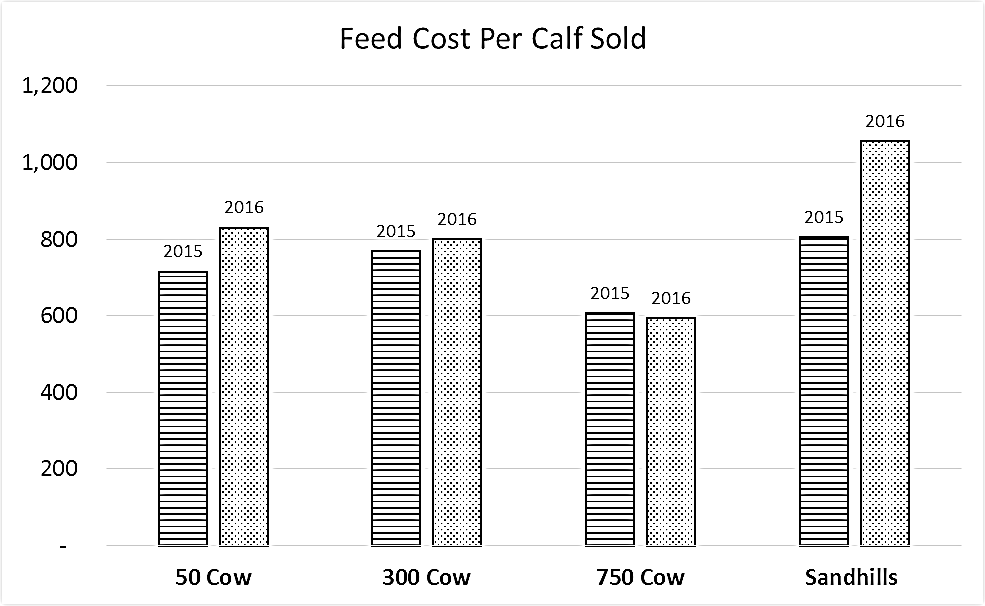

In addition to the decline in cattle prices from the 2015 to 2016 period, feed costs increased for three of the four budgets, with the Sandhills budget showing the greatest increase of $251 per calf. This is due to the large increase in the cost of leased grazing in the North Agricultural Statistics District, which includes Cherry County, and the fact that a large part of the feed in this budget comes from grazing. Grazing rate increases were calculated using data from the 2014-2015 Nebraska Real Estate Summary.

The 750-head Cow Herd System budget is the only one that shows a lower feed cost ($13 per calf) in 2016 compared to 2015. This lower cost is a result of lower hay prices, which makes up most of the winter ration.

The Sandhills budget showed the largest decrease in profitability, $916 per calf. Profitability on this budget declined from a positive $492 per calf in 2015 to a negative $424 loss in 2016. Lower cattle prices and higher feed costs explain all but $19 of this decline.

While the 750-cow budget, representative of the Central Agricultural Statistics District, is the only one of the published budgets showing a positive profit for 2016, $218 per calf, it has the second largest decline in profitability. The budget projects profit will decline by $563 per calf from the 2015 level of $780.

The 300- and 50-head cow budgets, representative of the Central Agricultural Statistics District and Northwest Agricultural Statistics District (Panhandle) respectively, have similar declines in profitability from the 2015 to 2016 period. The 300-cow budget declined $524 per calf while the 50-cow budget declined $534 over this period. The 2016 profits were budgeted at a negative $240 per calf for the 300-cow operation and a negative $289 per calf for the 50-cow operation.

While comparing these budgets over time provides insight into industry trends, it is important to remember there are substantial differences among firms throughout the state in the prices they pay for resources and the prices received when they sell their calves resulting in wide differences in profitability.

This is why it is important to modify any budget to reflect the ranch for which the budget is used. For example, budgets for ranches that primarily rely on grazing land owned by the firm may still show substantial profits given the present price structure. However, including a reasonable cost for those resources may show that much of that profitability is a return on land investment rather than operation profitability. The impact that lower profitability of cow-calf production will have on future grazing lease rates and sale prices for grazing land will be interesting to watch.

Roger Wilson

Budget Analyst, Farm Management

Dept. of Agricultural Economics

University of Nebraska-Lincoln

rwilson6@unl.edu

402-472-1771

Topic: