Content

February 25, 2026

Author: Jay Parsons, Center for Agricultural Profitability

According to USDA National Agricultural Statistics Service data, Nebraska had 38,300 acres planted to sunflowers in 2025 and 37,100 acres harvested (97% of acres planted). The average yield was 1,100 pounds per acre for a total production of 40.8 million pounds. This represents a significant increase (+45%) in production from 2024 driven by an increase in acres planted (+35%) and four percentage point increase in the percentage of planted acres harvested, which led to a 41% increase in total acres harvested.” Yield was also up about 2% on harvested acres.

While 2025 looks like a bright spot for Nebraska sunflower production, sunflower production has varied tremendously in Nebraska over the past 35 years. For example, in 1991, there were 50,000 acres planted to sunflowers in Nebraska, with the split between oil-type sunflowers and non-oil (confection) sunflowers being 60/40. Changes in farm bill legislation in the 1990’s led to an increase in sunflower acres that peaked in 1999 at 101,000 planted acres, which was almost evenly split between oil and non-oil. While somewhat volatile from year to year, planted acres remained as high as 99,000 acres in 2005 before a downward trend started that led to a low of 28,300 acres planted in 2024. However, even more striking than the decline in acres is the change in the mix of sunflower types planted. Unlike the more even split of the 1990’s and early 2000’s, oil-type sunflowers made up 94% (36,000) of the total sunflower acres planted in Nebraska in 2025.

Nebraska ranked sixth nationally in sunflower production in 2025, just above Kansas and slightly below Colorado. North and South Dakota dominate U.S. production of sunflowers making up 84% of the 2025 total. U.S. sunflower production has varied like Nebraska’s. Production for 2025 totaled 2.2 billion pounds nationally, a 103% increase over 2024. Like Nebraska, a substantial increase of 183% in harvested acres and a more modest increase in yield (10%) drove this increase in production. However, overall, Nebraska sunflower yield falls well short of the national average yield of 1,863 pounds per acre.

Going back to 1979, U.S. sunflower production peaked at 7.3 billion pounds on 5.5 million acres. In the late 1990’s, around five billion pounds were produced annually on about 3.5 million acres. Nationally, oil sunflowers made up 92% of the production in 2025. In 1999, oil sunflowers made up only 78% of the production.

Ukraine remains a top global producer and exporter of sunflower seeds and oil, despite war-related disruptions in production and transportation. However, overall sunflower production has declined in Ukraine by 35-40 percent since the pre-war levels of 2021. Global use of sunflowers remains steady while worldwide production has declined. This has led to declining global stocks with the 2025 ending stocks estimated at 2.8 million metric tons, a 4% decrease from 2024 and a 13% decrease from 2023. Furthermore, the ending stocks are projected to decline another 15% during this marketing year to reach a low of 2.28 million metric tons by the end of September 2026.

Tight supplies and steady demand are usually a recipe for higher prices. At the time of this writing, the price discovery process for 2026 crop insurance price elections is ongoing. However, USDA-RMA currently lists the projected price for oil type sunflowers at $29.00 per cwt. If realized, this would be a 25% increase over last year’s spring projected price of $24.00 and 11% higher than the 2025 harvest price of $26.20. A similar story exists for confectionary (non-oil) sunflowers. They are currently projected at $37.10 per cwt. That is up 15% from the 2025 spring projected price of $32.30 and 6% higher than the 2025 harvest price of $35.10.

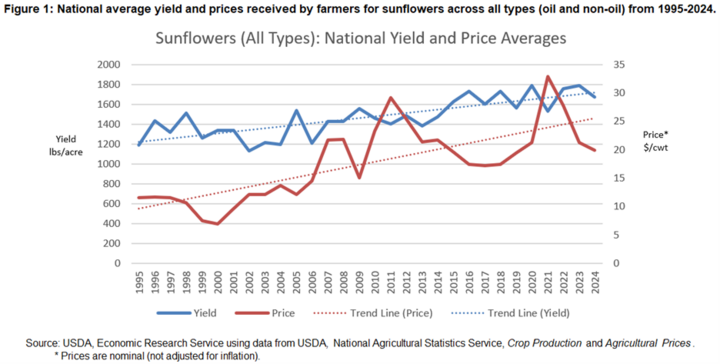

USDA ERS has maintained a data set for sunflower acreage, production, and prices since 1980. Figure 1 shows the national average price received for all types of sunflower seed versus the average yield for the last 30 years (1995-2024) based on harvest season. (Note: even though the 2025 harvest season is over, the average price received for the 2025-26 marketing year is yet to be determined.)

While both prices and yields have trended upward, the price received trended upward a little faster but with much more volatility. Yields have increased an average of seventeen pounds per acre per year over the 30 years while price has increased five and half cents per pound. However, the variation in year-to-year change in the price received by farmers on a percentage basis is ten times higher than it is for yield.

The increase in prices received and yield per acre for sunflowers over the last 30 years has led to a four-fold increase in the value of production per acre (Figure 2). However, because of the decrease in acres planted to sunflowers, overall revenue from sunflowers in the U.S. has changed extraordinarily little from 1995 to 2024. One of the big questions is whether this trend in declining acres will change with current market conditions. Sunflower acreage expanded notably in the 2025 crop year. Will we see another increase in 2026? Recent changes to the farm bill legislated reference prices passed last summer in the One Big Beautiful Bill Act (OBBBA) may also have a positive influence on sunflower production acres. Sunflowers share the reference price for “other oilseeds” in the farm bill, which increased 17.9% in the OBBBA from $20.15 to $23.75 per cwt. This was a larger increase than that of corn (+10.8%) or wheat (+15.5%) and similar to soybeans (+18.5%).

Summary and Outlook

Sunflower production in Nebraska and across the United States has experienced significant variability over the past three decades, influenced by shifting acreage, changing market dynamics, and evolving farm policy. The strong rebound in 2025—driven by higher planted acres, improved yields, and firm market prices—highlights the crop’s continued potential despite long‑term declines in acreage. Nationally, rising prices, tightening global stocks, and steady demand signal favorable conditions heading into 2026. Policy changes, including increased reference prices for oilseeds under the OBBBA, may further encourage planting decisions. Whether this momentum carries forward will depend on producer response to market signals, global supply conditions, and the broader economic environment for crop production.

Author Contact:

Jay Parsons, Professor

Director of the Center for Agricultural Profitability

Department of Agricultural Economics

University of Nebraska-Lincoln

jparsons4@nebraska.edu

402-472-1911