Cornhusker Economics Nov 1, 2023

Notes from the Brazilian Cornfields

By Fabio Mattos

{kind=link}

In the last few months, I have been traveling in Brazil. My objective with this trip is to meet with industry professionals, government officials, and academic researchers to learn about recent developments in Brazilian agriculture and what we can expect to see in the future. I have essentially been asking people their opinions about the main developments in Brazil in the last few years and their perspectives for the future. One of the main topics that has emerged consistently in these conversations is, not surprisingly, the corn market.

Let us go ahead and discuss the corn market in Brazil as we highlight the main ideas that have come up during my conversations. Just keep in mind that this is not a scientific study, but rather notes and information gathered from my conversations about agriculture in Brazil.

How many crops can we have in a year?

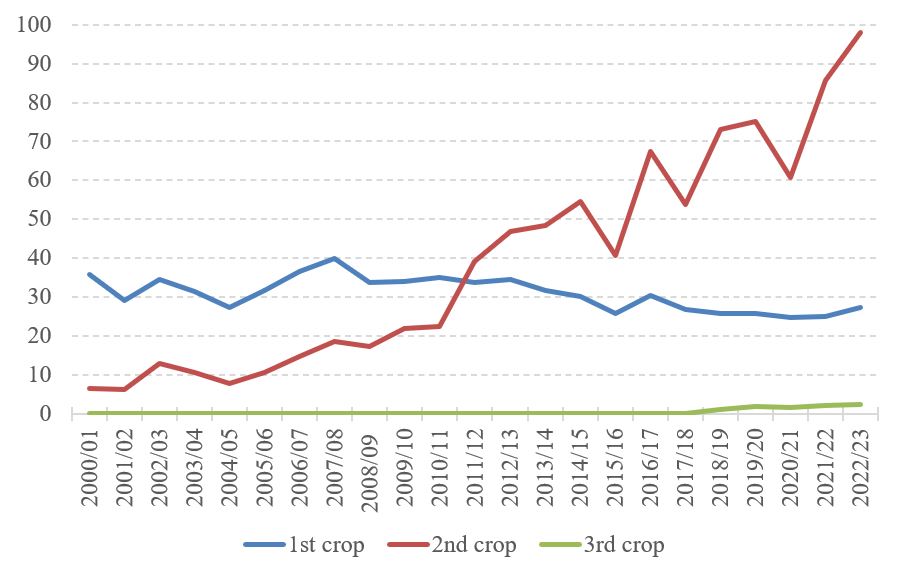

This is not quite new, but Brazil has now 3 corn crops in a year. The first one, more traditional, is planted in September-December and harvested in January-April. The second one, which started small years ago and is now the main crop, is planted in January-April and harvested in June-August. The third one, which started more recently, is planted in April-June and harvested in October-December. Figure 1 illustrates how the traditional 1st crop has lost ground while the 2nd crop has gained importance over the last 23 years. It also shows the emergence of the 3rd crop in the last few years. Based on the estimates for the 2022/23 crop year, the proportions of annual production that comes from each crop are: 21% from 1st crop, 77% from 2nd crop, and 2% from 3rd crop.

Figure 1: Corn production in Brazil (million tons) – 2000/01 to 2022/23

Source: Conab/Brazil (2022/23 is an estimate)

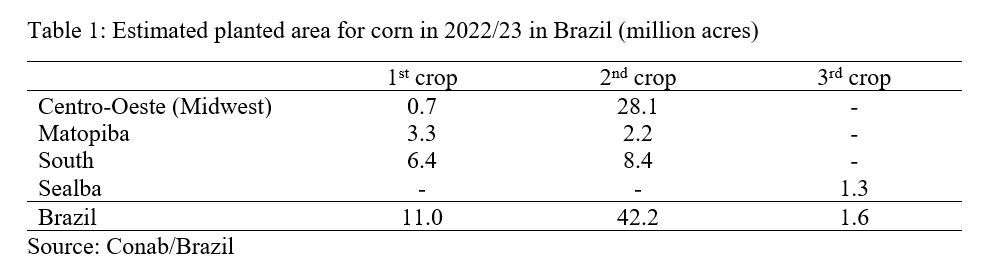

The three crops come mostly from different production areas in the country (Figure 2). The 1st crop is concentrated in the traditional production areas in the south. For 2022/23, it is estimated that 63% of the 1st crop will come from the south, followed by 22% coming from Matopiba (this is an acronym formed by the first letters of the states in the region: Maranhao, Tocantins, Piaui, and Bahia). The 2nd crop is concentrated in the “Centro-Oeste” (Midwest) region, which is currently the main production area in the country. For 2022/23, it is estimated that 73% of the 2nd crop will come from the “Centro-Oeste” and 19% will come from the south. Finally, the 3rd crop is concentrated in the newest (and smallest) production area in the country: Sealba, which is also an acronym formed by the first letters of its states (Sergipe, Alagoas and Bahia). For 2022/23, it is estimated that 90% of the 3rd crop will come from Sealba.

Figure 2: Corn production areas in Brazil

How much can the 3rd crop grow?

One point that came naturally in my conversations was how much more corn production in Sealba (3rd crop) can grow in the future. Let us think about this looking at planted area and yields. Table 1 shows estimated planted area for corn in 2022/23 across the main production areas for each crop. Sealba is already a smaller geographical area compared to the other production regions, which largely explains why its planted area is smaller compared to planted area in other regions. The questions then are whether more area in the region can be also used for corn and whether corn could expand to neighboring areas (such as further into Bahia or to the state of Pernambuco in the north). Opinions are mixed here. Overall, it seems to be unclear how much producers will be able to expand planted area in that region, i.e., whether it will be (financially) worth preparing new land or replacing other crops with corn.

Another dimension is the yield. Average yields in Sealba are still lower compared to other production regions (Table 2). Average yield in the region was 41.4 bushels/acre in 2018/19, then remained above 50 bushels/acre in the following years until reaching its highest value of 57.9 bushels/acre in 2022/23. What I heard is that there is certainly room to increase yields in the area, but there are again mixed opinions about how much it can increase. In general, people I talked to do not believe yields in Sealba can increase to the levels of the Centro-Oeste, or even close to that. It is true that Sealba is a new corn area. Even the Centro-Oeste, which is a Brazilian agricultural juggernaut, took some time to start growing strongly and increase yields significantly after it started producing grains. Still, at this point, people seem to be careful to bet on significant yield increase in Sealba.

Overall, people seem to be cautious about how much the 3rd corn crop can increase, but there seems to be a general expectation of increasing production in coming years. Currently, corn production in Sealba (3rd crop) is close to 2 million tons. Most people I talked to believe this number can reach 4-5 million tons in the next few years. In addition, the general opinion is that the 3rd corn crop will keep being directed to domestic consumption and not exports (which still means that an extra few million tons from other regions can be exported now).

How much more can grain production grow?

Another point that came naturally in my conversations was how much more corn production in the whole country, as well as grain production in general, can grow in coming years. Most people agree that there is large room for expansion in planted area in the country. There are different opinions about how much each production region can grow, but the general opinion is that there is room for growth in all regions and especially in the Centro-Oeste.

They emphasized that growth could come from two main fronts. One is to make more intensive use of cattle pasture, freeing some land to plant grains. Another front is to recover degraded pasture. It is estimated that there are approximately 220 million acres of degraded pasture in Brazil, mostly in the Centro-Oeste and the area north of it. In 2022/23, 194 million acres of grain crops were planted in Brazil, hence the area with degraded pasture is 13% larger than the planted area for grains in 2022/23.

Nobody seems to have a good idea of how much of degraded pasture will be recovered and how much of that will be used for grain crops since these decisions depend largely on the cost of recovering pasture and the potential profit of growing more grains in those areas. As a simple exercise, if we assume that ¼ of degraded pastures are recovered in the next few years and used to plant corn and soybeans, this will represent an increase of 28% in planted area for corn and soybeans, which also points to a large increase in production in this scenario.

People I talked to have been working on this kind of exercise trying to figure out how much grain production can increase in Brazil. The outcomes from these analyses vary greatly depending on their assumptions. Overall, what I heard is that there is a potential to increase corn and soybean production in Brazil by 50% to 100%. Note that “potential” is the keyword here. They don’t necessarily believe that such an increase will actually happen in the near future, but rather that it could happen if and when all factors line up properly at the right time.

What else have I heard in the cornfields?

Two other points have emerged frequently in my conversations here in Brazil. One of them is logistics. Shipping grain from production areas to export ports or to domestic consumption areas is still a challenge. However, important developments have taken place in the recent past and the dynamics of transportation in Brazil have been changing, making it relatively easier, faster, and cheaper to move grain around the country. There is still a long way to go, but there are clear improvements happening in the country.

New developments in the production of ethanol and biodiesel have also come up regularly, especially the expansion of ethanol from corn (instead of ethanol from sugarcane, which has been traditionally produced in Brazil). Ethanol from corn already corresponds to about 15% of total ethanol production in Brazil and the expectation is that the proportion will keep increasing.

We are running out of space here, so we will leave these two topics for future articles. Stay tuned to our Cornhusker Economics!